![Millennials Are Killing…It! [2021 Study in Defense of the Millennial]](https://cdn-images.zety.com/pages/millennials-are-killing-it-ztus-cta-02.webp)

Table of Contents

Millennials killed marriage—how dreadful! Millennials also killed divorce—how dare they?!

And just when you thought that it couldn’t get any worse, the newly discovered coronavirus COVID-19 is reeking havoc across the entire world. And yep, Millennials are to blame for spreading it.

No matter the problems that you or the country have been facing, they all seem to have one, singular source of blame—Millennials.

“Millennials are killing *spins wheel*” has been used so often and for so many of the current world’s pains and troubles that you would have heard of it—even if you were living under a rock all this time. And that’s probably the Millennials’ fault too.

Living in a hyped up world constantly blaming Millennials for everything that’s changing, we got to thinking—do people actually believe any of this is true? And is it true to begin with?

So we asked 1000 Americans about what they thought about Millennials to see if they bought into the stereotypes they’re constantly bombarded with. And then juxtaposed that with reality. Here’s what we learned.

Family Ties or Family Noose?

One of the worst crimes Millennials have been accused of has been the disruption of the modern family primarily through the fall in the number of marriages and a rise in divorce rates.

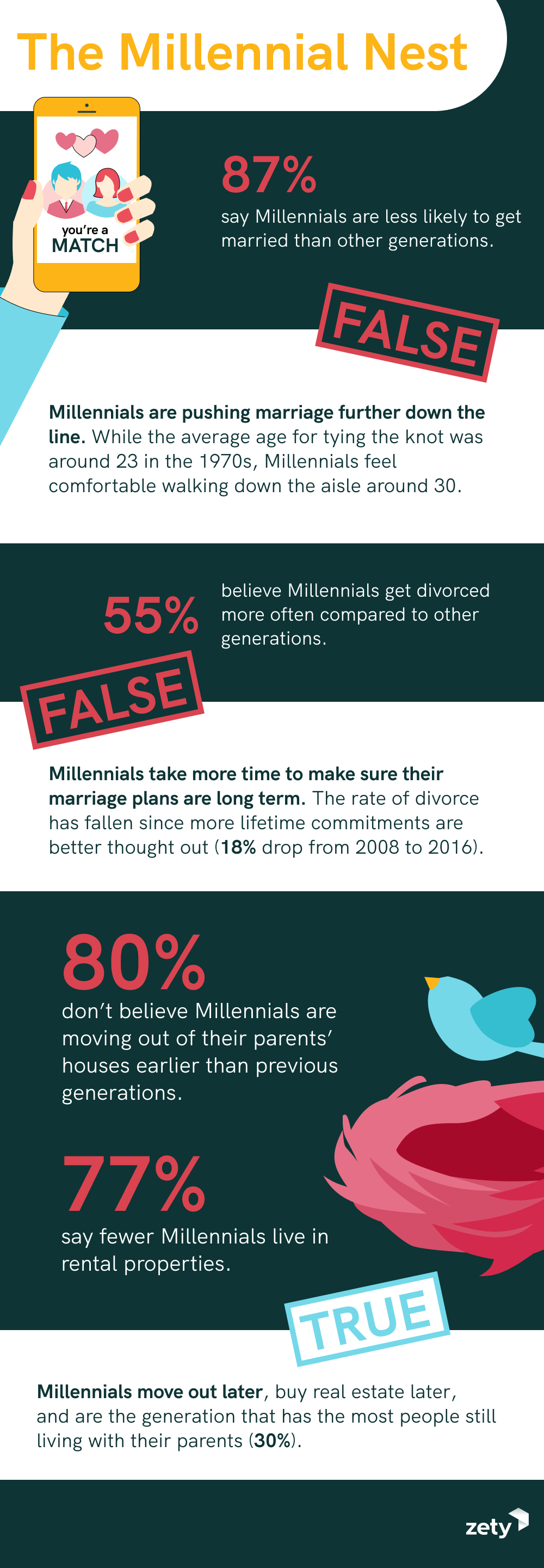

A resounding 87% believe that Millennials are less likely to get married than other generations. It’s no surprise that Baby Boomers led the way with 93% saying that Millennials are in no hurry to get hitched.

So what about divorce? Respondents seemed to be more understanding here, but still 55% believed that Millennials get divorced more often compared to other generations.

How does that stack up according to statistics?

FALSE!

According to Goldman Sachs, Millennials haven’t given up on marriage, they’re just pushing it further down the line. While the average age for tying the knot was around 23 in the 1970s, Millennials feel comfortable walking down the aisle around 30.

A study by a University of Maryland professor suggests that since Millennials take more time to make sure their marriage plans are long term, the rate of divorce has fallen since more lifetime commitments are better thought out (18% drop from 2008 to 2016).

With that in mind, you could argue that Millennials are making sounder choices than generations past, which is a good thing.

The Parents’ Home is the Millennials’ Castle

The housing market is floundering because Millennials don’t feel like leaving the family nest any time soon. It’s that simple.

Or is it?

80% of respondents don’t believe Millennials are moving out of their parents’ houses earlier than previous generations. Nearly the same amount go on to think that Millennials are renting more than their predecessors.

Whether renting or buying, everyone knows that one of the key factors is location, location, location. In the never ending battle between the city and the suburbs, only 20% believe the ‘burbs are where Millennials like to chill when they’re not busy killing things.

The thing is—that’s TRUE!

But these numbers need to be put into context before anyone runs off to scream at Millennials to finally move out.

The Pew Research Center points out that Millennials may be moving out later, buying even later, and happier to live in urban areas, but a lot of that is due to the Great Recession that hit Millennials particularly hard.

Soaring prices and wages that aren’t soaring at all have Millennials forced to put off buying their own abode simply due to a lack of funds. Millennials are, in fact, the generation that has the most people still living with their parents (30%).

And those aren’t the only reasons.

Cap and Gown, Ball and Chain

Graduating from college gives you two things—a higher education and even higher financial debt.

But every generation has gone to college so Millennials are in the same boat as any other generation, right?

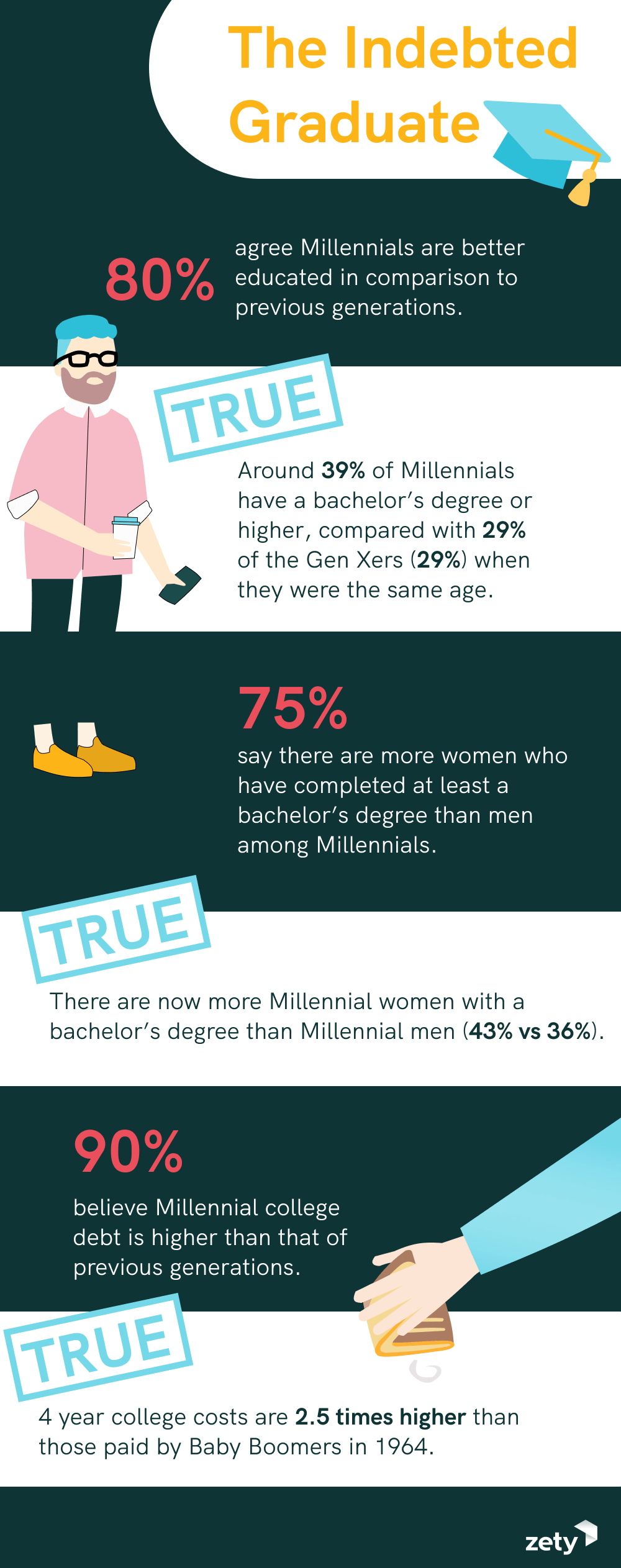

Well, nearly 80% of respondents believe that Millennials are actually better educated than previous generations. It’s also worth noting that more than 70% of respondents correctly identified a positive trend—the amount of women with at least a bachelor’s degree exceeds that of men.

So are Millennials having a better college experience than previous generations—TRUE!

But that doesn’t mean that they’re better off because they’re better educated. Truth be told, the main factor is not only the degree Millennials obtain, but also the financial burden they need to shoulder.

In the end, a better education equals more and higher college debt. Almost no one (10%) believed that Millennial college debt is lower than that of previous generations.

And they’re absolutely correct.

Indeed, according to the AARP Public Policy Institute, when adjusted for inflation, 4 year college costs are 2.5 times higher than those Baby Boomers paid in 1964.

If you take that data and add on the fact that student loan debt is the second highest credit debt in the United States (mortgage loan debt being first), it begins to paint a clearer picture of why Millennials are so slow to buy their own home and why they pay such close attention to the economy.

Which leads us to our next questions.

Toss a Coin to Your Millennial

Word on the street is that when Millennials aren’t busy happily hacking away at another cornerstone of American culture, they’re quite lazy.

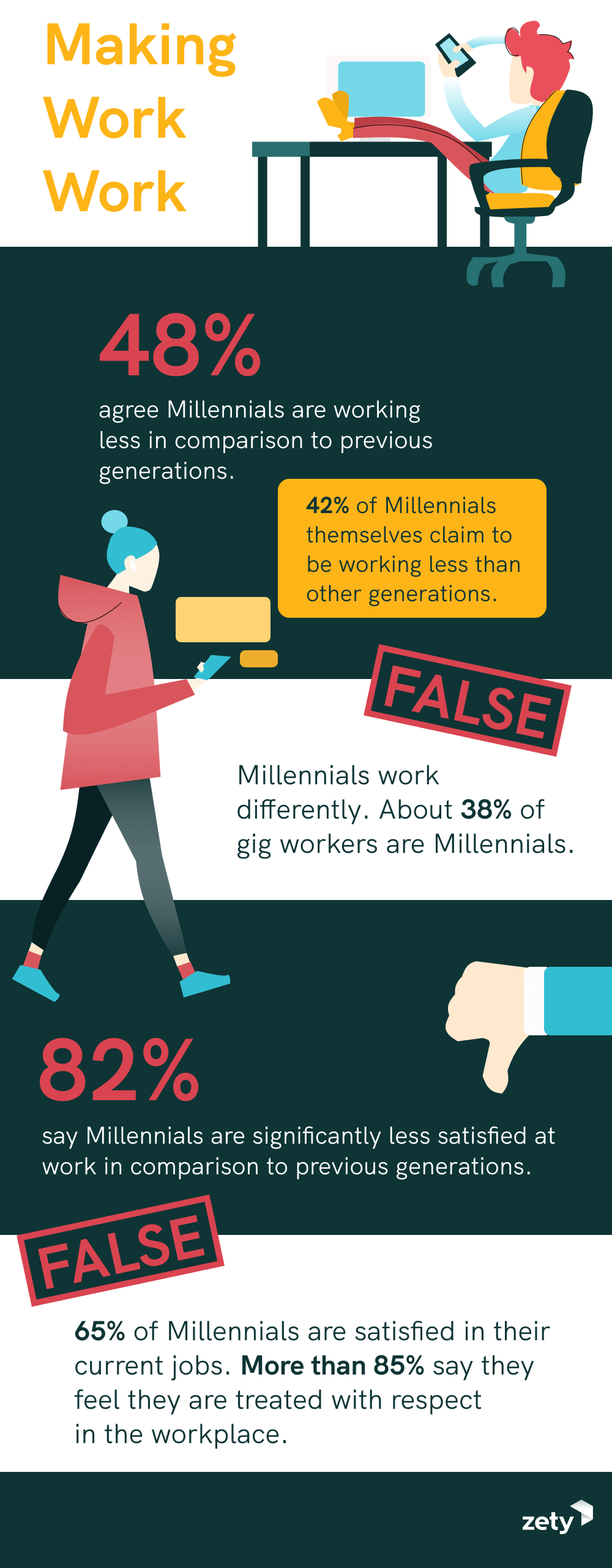

At least that’s what about 50% of respondents think. Interestingly enough, 42% of Millennials themselves claimed to be working less than other generations.

FALSE! says the economy.

Millennials might actually be a case of not working less, but just smarter.

The economy has adapted along with the Millennial generation, primarily driven by advancements in technology and the massive shift towards a gig economy. In fact, it’s estimated that about 38% of gig workers are Millennials.

In other words, the way of working has changed drastically compared to the Baby Boomer generation and having a normal 9 to 5 is no longer the norm nor is it something everyone wants.

This may account for why Baby Boomers, out of all the generations, were most inclined to agree with the statement that Millennials work less than they did.

But things start to get even trickier when we asked more specific questions about how Millennials put food on the table.

72% of respondents thought that Millennials were more likely to pack up a U-Haul and hightail it to a job somewhere else than previous generations. That’s quite close to the 65% who believe that the paycheck rules more supreme over a Millennial than their predecessors.

But despite this inclination to sacrifice a lot for their career, people seem to think that Millennials aren’t all that happy doing it.

62% of respondents believe that Millennials don’t feel that their job is as important a part of their life as it used to be for previous generations. It goes even further with 82% convinced that Millennials get a lot less satisfaction out of work than their predecessors.

Millennials are known as the most job-hopping generation to date, so they must not care about their jobs and be unhappy. Right?

NOPE!

Boston College data suggests that careers are very important to the majority of Millennials. In fact, a vast majority of Millennials are willing to go over and beyond what’s expected of them in the workplace to be successful.

The thing is, Millennials put a lot more value on everything surrounding their job than previous generations. Just having a job isn’t a reason to stay on with the same employer for a long time.

A study by EY underlines this fact, pointing out that Millennials reciprocate company flexibility and benefits with loyalty, happiness, and engagement.

Millennials simply put more emphasis on everything outside their salary and those are the factors that usually cause them to change jobs. And given they buy houses and have families at a later age compared to previous generations, Millennials have the liberty to relocate for a new job.

Employers take heed—according to a Gallup report, one of the major reasons leading to Millennial job hopping is the fact that they simply don’t feel engaged in their work. If the job’s not worthwhile, a Millennial will find another.

Netflix and Chill with Mary Jane

Experimentation among young people is almost like a tradition. A tradition dictates that Millennials should be into alcohol, tobacco, drugs, and sex.

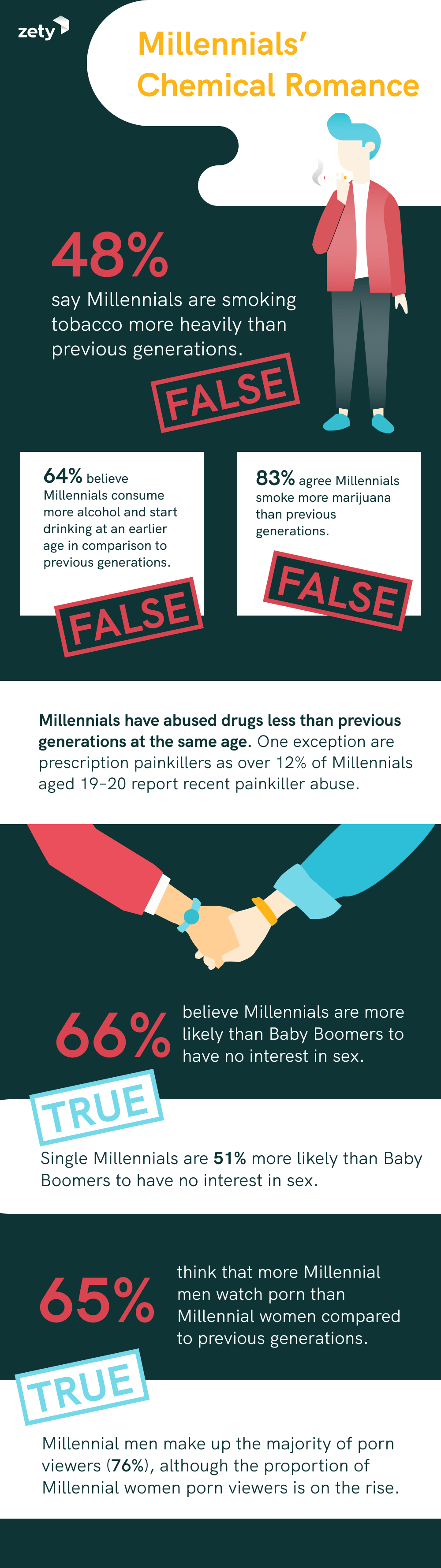

But when asked, a little more than 80% of respondents stated that Millennials smoke less than previous generations.

It turns out the positive thinking stopped there.

More than half of respondents believe that Millennials are taking to the bottle more than previous generations. Interestingly enough, healthcare professionals were 10% more inclined to agree with this than others.

An overwhelming 83% of respondents believe Millennials are puffing away at Mary Jane more than previous generations. In fact, respondents believe that marijuana was the Millennials’ go to narcotic.

What do the numbers say?

WRONG!

Millennials have actually abused drugs (cocaine, hallucinogens, psychotherapeutics, tranquillizers, sedatives, stimulants, heroin, marijuana, alcohol) less than previous generations at the same age.

The only exception to this trend is prescription painkillers which, sadly, are the Millennials’ drug of choice. Over 12% of Millennials aged 19-20 report recent painkiller abuse.

So if Millennials aren’t constantly stoned or plastered, maybe they’re having their fun between the sheets?

66% of survey takers believe that Millennials are more likely than Baby Boomers to have no interest in sex. Nada. Zero. Zilch.

65% go on to think that more Millennial men watch porn than women compared to previous generations.

CORRECT!

Single Millennials are 51% more likely than Baby Boomers to have no interest in sex at all.

Also, Pornhub data confirms that men make up the majority of porn viewers. The interesting thing is that the proportion of women porn viewers among Millennials is on the rise!

Key Takeaways

In the end, it turns out that people don’t have the entire picture when it comes to Millennials. While everyone is chanting about the next great thing Millennials are killing, real data suggests that Millennials are really killing it.

Each generation has its own characteristics and its badges of economic and social change. Perhaps it would be better for everyone to simply call it change (or progress if you’re really passionate about it) and put the axes and knives away.

Methodology and Limitations

In this study, we collected answers from 1,013 Americans via Amazon’s Mechanical Turk. Respondents consisted of 59.3% females and 40.7% males.

This self-report study investigated what stereotypes Americans believe in when thinking about Millennials. Those were then juxtaposed with the realities Millennials face and the context in which they live.

Respondents were asked 23 questions, the majority of which were yes/no or select one.

The data collected suggests that most of Americans’ understanding of Millennials relies heavily on stereotypes and not real studies and data.

Fair Use Statement

Feel free to share our study! The content found here is available for non-commercial reuse. Just make sure to link back to this page to give the authors proper credit.

Sources

- Philip N. Cohen. The Coming Divorce Decline

- Richard Fry, Americans are moving at historically low rates, in part because Millennials are staying put

- Kristen Bialik and Richard Fry, Millennial life: How young adulthood today compares with prior generations

- Joe Valenti, A Look at College Costs across Generations

- Brad Harrington et al., How Millennials Navigate Their Careers: Young Adult Views on Work, Life and Success

- Hiring Millennial Talent in 2019: A report on attracting and retaining this generation | LaSalle Network

- Amy Adkins, Millennials: The Job-Hopping Generation

- Coming of Age: Millennials | PornHub Insights

- Drug and Alcohol Abuse Across Generations | Drugabuse.com

- Singles in America: Match Releases Largest Study on U.S. Single Population | Match

About Us

Zety supports entry-level candidates with specialized guides just for them. Our experts provide tips on how to write a resume without experience, highlight education and include interests in a job application, and where to find free Google Docs resume templates.

About Zety’s Editorial Process

This article has been reviewed by our editorial team to make sure it follows Zety’s editorial guidelines. We’re committed to sharing our expertise and giving you trustworthy career advice tailored to your needs. High-quality content is what brings over 40 million readers to our site every year. But we don’t stop there. Our team conducts original research to understand the job market better, and we pride ourselves on being quoted by top universities and prime media outlets from around the world.

Share: